Year-End Accounting Checklist for Businesses: A Complete Guide to Financial Closing Before March 31

Financial year end is one of the most critical periods for any business. As March 31 approaches, companies shift their focus from daily operations to financial accuracy, compliance, and reporting. Year end accounting is not just about closing books, it is about ensuring that every financial detail reflects the true position of the business. Errors at this stage can affect tax filings, audits, and future planning.

Many businesses struggle during this time due to incomplete records, rushed reconciliations, or lack of structured processes. A well defined year end accounting checklist helps reduce stress, improves accuracy, and ensures that financial closing happens smoothly. Whether it is a small business or a growing organization, disciplined financial closing practices are essential for long term stability.

Year end accounting also plays a key role in decision making. Accurate financial data helps leadership understand performance, identify gaps, and plan for the next financial year. Without proper closing, businesses may rely on incorrect data, leading to poor financial decisions.

What Is a Year End Accounting Checklist and Why Is It Important

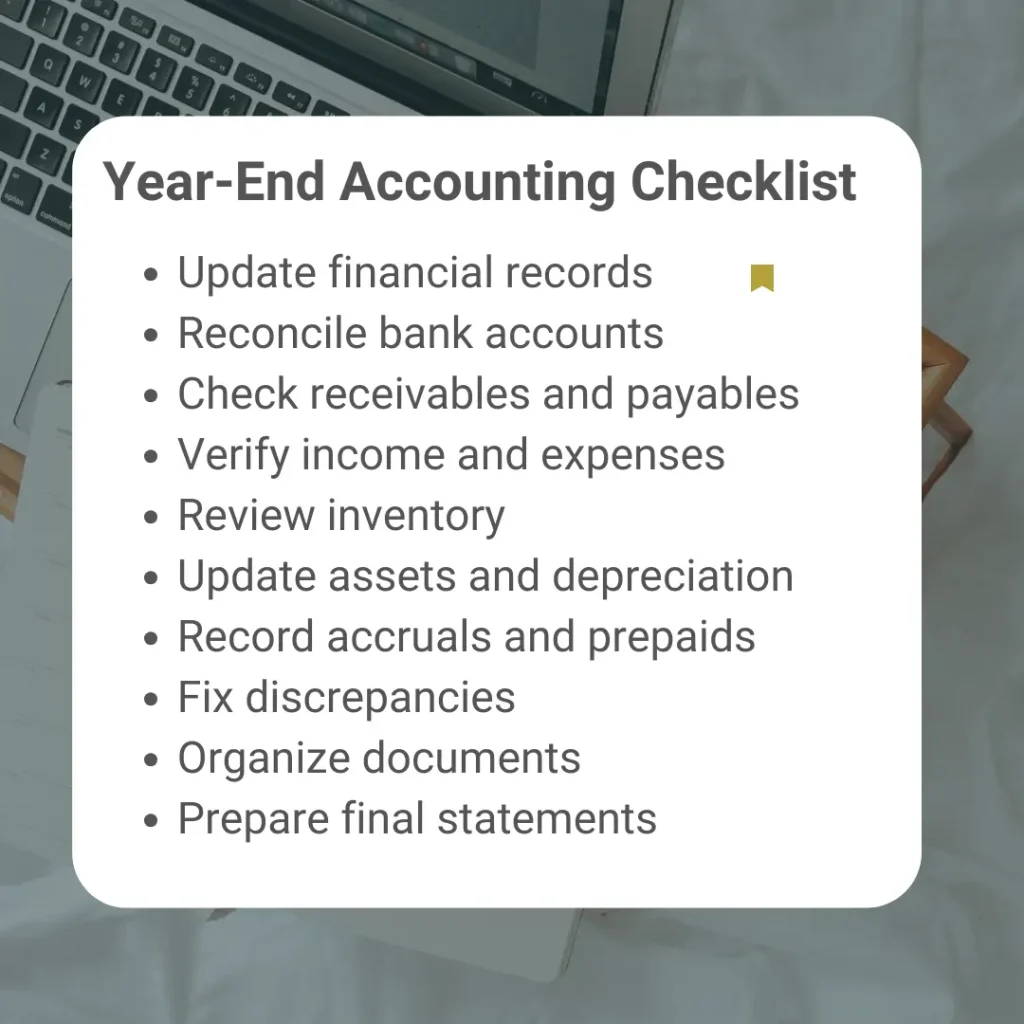

A year end accounting checklist is a structured list of tasks that businesses must complete before closing their financial books. It ensures that all transactions are recorded, reconciled, and verified before preparing final financial statements.

The importance of this checklist lies in consistency and accuracy. Without a checklist, teams may overlook key tasks such as account reconciliation, expense classification, or compliance requirements. This increases the risk of financial errors and delays in reporting.

A proper checklist also helps businesses stay aligned with statutory requirements. It ensures that records are ready for tax filing and audits. More importantly, it builds confidence in financial data, which is essential for internal and external stakeholders.

Why Do Businesses Face Challenges During Year End Closing

Year end closing often becomes stressful because multiple tasks need to be completed within a limited timeframe. Many businesses delay accounting reviews throughout the year and then try to fix everything at the end.

Common challenges include:

- Incomplete or missing financial records

- Delays in bank and ledger reconciliations

- Misclassification of expenses and income

- Lack of coordination between departments

- Errors in financial data entry

- Unclear documentation for transactions

These challenges increase the chances of inaccurate financial reporting. When businesses do not follow a structured year end accounting checklist, they often face last minute confusion and compliance risks.

What Should Be Reviewed Before Closing Financial Books

Before finalizing accounts, businesses must review all financial records to ensure accuracy and completeness. This step is essential to avoid discrepancies in financial statements.

Key areas to review include:

- Revenue recognition to ensure all income is recorded correctly

- Expense classification to avoid misreporting

- Outstanding receivables and payables

- Inventory valuation and adjustments

- Fixed asset records and depreciation

- Loan balances and interest calculations

A detailed review helps identify errors early and ensures that financial statements reflect the correct position of the business.

How to Reconcile Accounts Effectively at Year End

Account reconciliation is a key step in year end accounting that ensures internal records match external statements like bank accounts, customer balances, vendor statements, tax returns, and intercompany transactions. Regular reconciliation helps reduce discrepancies, improves financial accuracy, and makes the audit process smoother and faster.

What Are the Key Adjustments Required in Year End Accounting

Year end accounting involves several adjustments to ensure that income and expenses are recorded in the correct financial period. These adjustments are necessary for accurate financial reporting.

Some common adjustments include:

- Accruals for expenses that are incurred but not yet paid

- Prepaid expenses that need to be allocated correctly

- Depreciation of fixed assets

- Inventory adjustments based on physical counts

- Provision for doubtful debts

These adjustments help align financial records with actual business performance. Without them, financial statements may present an incomplete or misleading picture.

Why Is Documentation Important During Financial Closing

Proper documentation is critical during year end accounting. Every financial entry should be supported by valid documents such as invoices, contracts, and receipts.

Strong documentation helps in:

- Verifying transactions during audits

- Supporting tax filings

- Reducing the risk of compliance issues

- Improving transparency in financial reporting

Businesses that maintain organized records throughout the year find it easier to complete year end closing without delays. Poor documentation, on the other hand, can create confusion and increase audit risks.

How Can Businesses Prepare for Year End Accounting in Advance

Preparation is the key to a smooth financial closing. Businesses that start early can avoid last minute pressure and reduce errors.

Some practical steps include:

- Maintaining updated accounting records throughout the year

- Conducting periodic reconciliations

- Reviewing financial data quarterly

- Ensuring proper classification of transactions

- Keeping all supporting documents organized

Early preparation not only simplifies year end accounting but also improves overall financial management.

How Does Year End Accounting Impact Tax Filing and Compliance

Year end accounting directly influences how accurately a business files its taxes. Financial statements prepared at the end of the year form the base for tax calculations. If there are errors in revenue, expenses, or adjustments, they will carry forward into tax filings.

Accurate financial closing ensures that taxable income is calculated correctly. It also helps businesses claim eligible deductions without errors. Poor year end accounting can lead to underreporting or overreporting of income, both of which may result in penalties or additional scrutiny.

Compliance is another critical aspect. Businesses must meet regulatory requirements, maintain proper records, and ensure timely submissions. A well executed year end accounting checklist supports smooth tax filing and reduces compliance risks.

What Are Best Practices for a Smooth Financial Year End Closing

A smooth year end closing process depends on planning, coordination, and consistency. Businesses that follow structured practices are able to complete financial closing efficiently without unnecessary delays.

Best practices include:

- Creating a clear year end accounting checklist and timeline

- Assigning responsibilities to specific team members

- Reviewing financial data regularly instead of waiting until year end

- Using accounting systems to track and organize data

- Conducting internal reviews before finalizing accounts

- Ensuring all reconciliations and adjustments are completed

These practices help reduce errors, improve accuracy, and ensure that financial statements are reliable.

Conclusion

Year end accounting is more than just a routine process. It is a critical step that determines the accuracy of financial reporting, the reliability of tax filings, and the overall financial health of a business. Without a structured approach, businesses may face errors, delays, and compliance challenges.

By following a well defined year end accounting checklist, reviewing financial records carefully, and maintaining proper documentation, companies can ensure a smooth financial closing. Preparation, consistency, and attention to detail are the key factors that make this process effective.

As businesses move into a new financial year, accurate year end accounting provides a strong foundation for better planning, improved decision making, and sustainable growth.

Quick Answers on Year End Accounting

What is a year end accounting checklist for businesses

A year end accounting checklist for businesses is a structured list of tasks such as reconciliation, adjustments, and documentation review to ensure accurate financial closing before March 31.

How can businesses prepare for year end accounting in advance

Businesses can prepare by maintaining updated records, conducting regular reconciliations, organizing documents, and reviewing financial data periodically.

Why is account reconciliation important at year end

Account reconciliation ensures that financial records match actual balances, reducing errors and improving the accuracy of financial statements.

What are common mistakes in year end accounting

Common mistakes include missing transactions, incorrect expense classification, delayed reconciliations, and lack of proper documentation.

How does year end accounting affect tax filing

Year end accounting impacts tax filing by determining taxable income, ensuring accurate reporting, and helping businesses comply with regulations.

What adjustments are required during financial year end closing

Adjustments include accruals, prepaid expenses, depreciation, inventory changes, and provisions for doubtful debts.

How can businesses ensure accurate financial closing

Businesses can ensure accuracy by following a checklist, maintaining proper records, reviewing data, and implementing internal controls.

What is the benefit of a structured year end accounting process

A structured process improves accuracy, reduces errors, ensures compliance, and supports better financial decision making.